When saving for a long-term goal, such as retirement, is it better to save small amounts for a long time, perhaps saving when we can ill-afford to, or waiting until later in life and putting larger amounts aside when it is more affordable?

This question has plagued society for decades and I fully understand the dilemma it presents.

So, let’s look at both sides of the debate and put some simple figures together.

At the outset, let’s set some ground rules in place:

- The savings are non-concessional (i.e. after-tax) contributions made to a superannuation fund.

- The rate of return earned is a net return (i.e. after the deduction of all fees, taxes, and charges).

- All projections are expressed in 2018 dollars. However, there will be inflation. This can be managed by increasing the amounts saved in line with inflation.

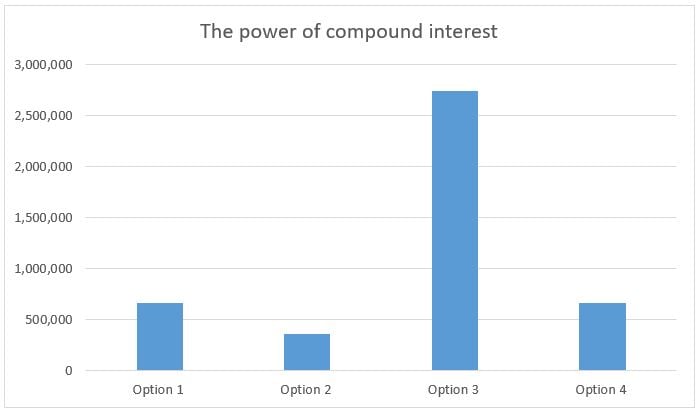

Option 1 - Saving $100 per week for 40 years, earning 5% per annum.

We will start saving $100 per week, from age 25 through to age 65. We earn a conservative 5% per annum of our savings.

According to the ASIC’s Moneysmart Calculator, we would accumulate a total of $661,275 over a 40-year period.

The actual savings contributed, amounts to $208,000 and the earnings component is more than double that at $453,275.

Option 2 - Saving $200 per week for 20 years, at 5% per annum.

In this option, we save $200 per week, but don’t start until age 45, also saving through to age 65, and earning 5% per annum.

In this instance, the amount saved will also be $208,000, however by starting later, the earnings are only $148,229, making a total of $356,229 after 20 years.

To achieve the same outcome as Option 1, we would need to save $371 per week from age 45 for 20 years.

But hypothetically, what if we earn 10% per annum instead of earning 5% per annum. After all, investing for 45 years, or even for 20 years, is long-term investing.

Between 1900 and 2017 the All Ordinaries Index of the Australian Stock Exchange returned an average of 13.2% per annum. The highest return of 66.8% was achieved in 1983, and the lowest return -40.4% was in 2008. In fact, over the 117-year period, 96 years returned a positive result and 22 years had a negative result.

But let’s return to the results.

Option 3 - Saving $100 per week for 40 years, earning 10% per annum.

The total amount saved is still $208,000, however, the total amount saved has jumped to a massive $2,740,434!

Sounds too good to be true, doesn’t it? Don’t worry, I ran the calculations a second time to check.

Option 4 - Saving $200 per week for 20 years, at 10% per annum.

Sadly, the accumulated savings after 20 years, even at 10% per annum, is a rather paltry $658,120.

So, the jury is in…...

Saving a smaller amount for a longer period certainly seems to win out.

In the words of Albert Einstein

‘Compound interest is the most powerful force in the universe’

comments